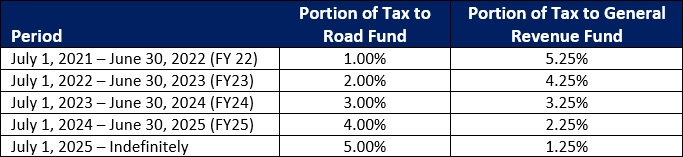

Beginning July 1, 2021, revenues from the sales tax on motor fuels will incrementally move over a 5-year period to the Road Fund. As summarized below, revenues from the 6.25% sales tax will gradually shift to funding transportation, in 1% increments up to 5%.

The sales tax on motor fuels is prepaid by each motor fuel retailer when purchasing fuel. The sales tax comes in the form of a cents per gallon rate, which is established by the Illinois Department of Revenue on January 1 and July 1 of each year. The rate is calculated by using the average selling price per gallon of motor fuel sold in the state during the previous six months and multiplying that rate by 6.25% to determine the cents per gallon rate (35 ILCS 120/2d). See the Illinois Department of Revenue website for current sales tax on motor fuel rates.

Sources: IL Dept. of Revenue (Gallons and Sales Tax Rates)

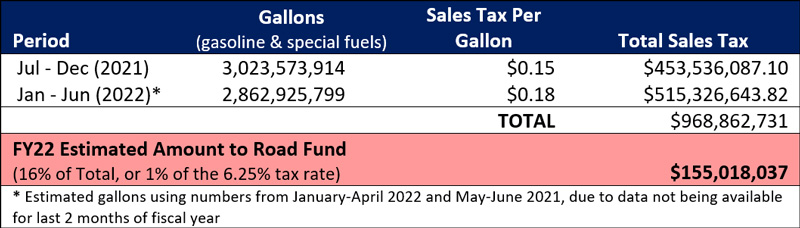

As summarized in the table below, it is estimated that $155 million of revenue from the sales tax on motor fuel was transferred to the Road Fund in FY 2022. This is 16% of the total annual sales tax on motor fuel, which represents the 1% going to the Road Fund out of the total 6.25% sales tax. This amount will increase each year until July 1, 2025.

Sources: Calculated using IL Dept. of Revenue values for gallons and tax rate